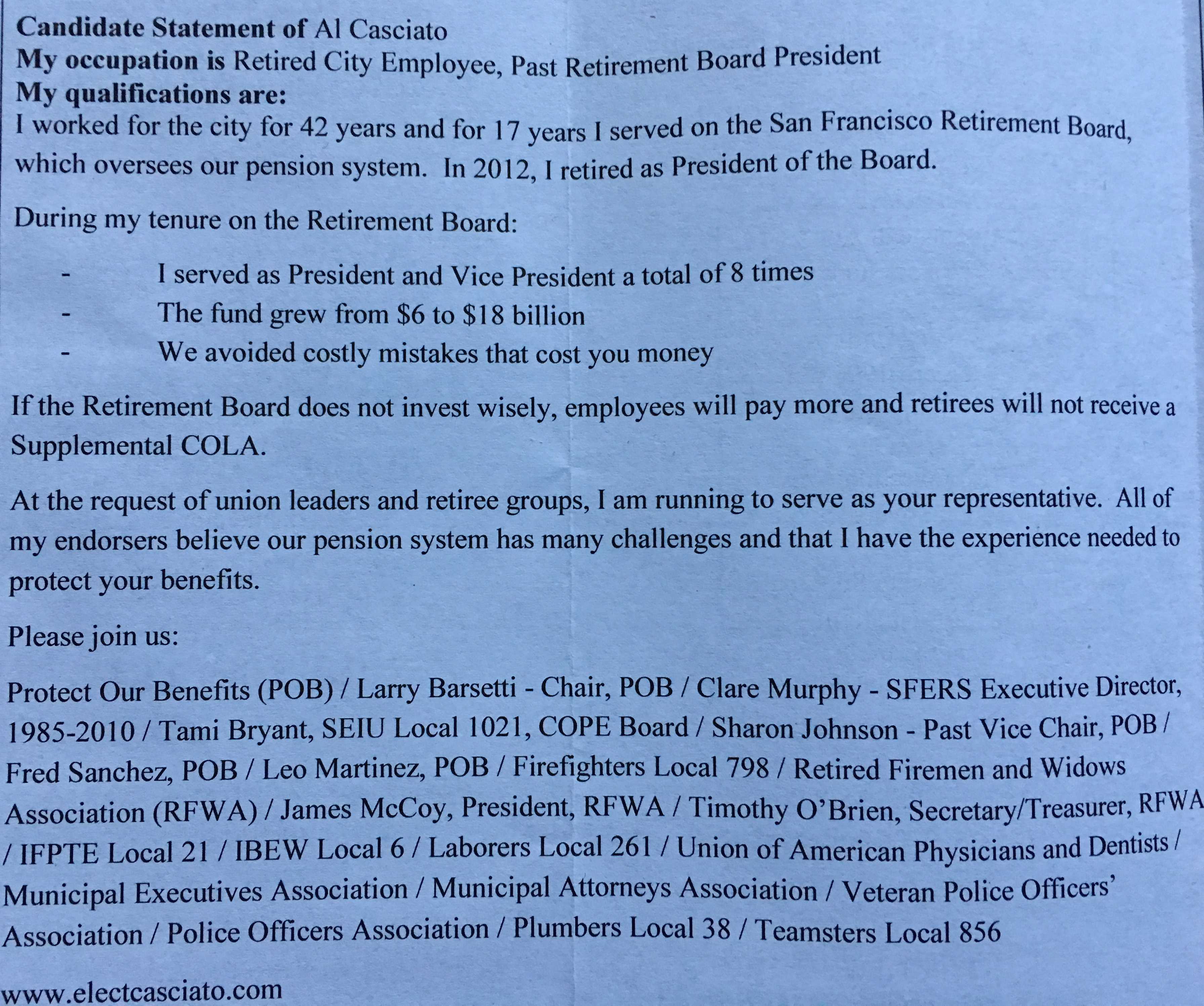

From the Open-Publishing Calendar

From the Open-Publishing Newswire

Indybay Feature

SFPOA Covering Up Take-Over Funding Of SFERS And Calls For Transparency From Malia Cohen

The San Francisco Police Officers Association is running a secretly funded campaign to seize control of the $20 billion San Francisco active and retired pension plan. They want 25% of the pensions invested in secret hedge funds and are keeping their campaign contributions secret. They contributions to the SFPOA's pension grab likely include hedge fund operators who could make millions for the vulture speculators. Even SF Supervisor Malia Cohen is calling for more transparency legislation to require that SFERS pension board elections funding information be made public.

Divisive election for SF retirement board election highlights transparency concerns

San Francisco Employees’ Retirement Board Member Herb Meiberger poses for a portrait Tuesday, January 3, 2016. (Jessica Christian/S.F. Examiner)

By Jonah Owen Lamb on January 15, 2017 1:00 am

The election for a seat on a little-known body that has power over billions of dollars in investments is getting ugly and the results could impact thousands of San Francisco pensioners, city coffers and taxpayers.

But no one knows how much money is being spent or who is paying for the campaign, which has prompted Supervisor Malia Cohen to introduce a drafting request for legislation that would require transparency in such elections.

But for now, this fight over a seat on the San Francisco Employee Retirement System will remain in the dark even though the seven-member body — three mayoral appointees, three elected seats and one Board of Supervisors appointee — collectively vote on how more than $20 billion in pension funds are invested.

So far, the two candidates — one a former cop and the other an incumbent and former city employee — have thrown accusations at one another in an uncommonly expensive race (almost $50,000 has been spent so far) that has included a protest in front of the San Francisco Police Officer Association and that body’s vocal support for one candidate.

Former SFPERS board member and retired police officer Al Casciato said he was called on by a number of city unions to run for the seat in order to remove the incumbent, who his campaign has called divisive and overcautious, and whose actions have already impacted the fund’s bottom line.

Herb Meiberger, the incumbent whose terms ends Feb. 20 and who worked for The City advising it on investing, has served on the SFPERS board for 24 years, said his role has been to keep steady the finances of the fund.

Meiberger has cast his opponent as a big spending police and fire union-backed candidate set on making riskier bets with the billions in investment dollars the retirement board controls.

Casciato’s election, Meiberger added, would put all three elected board members into the hands of public safety-linked members, which in other cities has not worked out well for pensioners.

The truth, at least the facts that can been pinned down in an election for which only public employees and retirees can vote and that is not required to be transparent like elections for public office, lies somewhere in between these narratives.

This all matters to city voters because the fund’s ultimate performance will be a major factor in how much The City must pay out in pensions.

The City projects a deficit of $119 million in the next fiscal year and $283 million in the subsequent fiscal year, which is driven largely by pensions and payroll. Those pension costs are projected to rise; by fiscal year 2021-22 The City expects to spend $431 million in pensions, $171 million more than previously expected.

The fund

The fund was valued at $21 billion as of fiscal year 2016-15, which is nearly $5 billion more than it was valued at in 2011-12.

Still, several recent years of less-than-robust gains have meant increased contributions from employees and The City.

This issue of how well the fund has been performing is at the heart of this divisive election, said Patrick Monette-Shaw in a recent San Francisco Examiner opinion article on the matter.

“They’re lying to frighten voters into voting for Casciato to invest more of SFERS’ $21 billion portfolio in high-risk hedge funds,” the West Side Observer columnist wrote.

But not everyone is siding with Meiberger, the incumbent.

A video attacking Meiberger on the POA’s website says his obstructionism has lost the fund money and cost benefits.

The candidates

Meiberger claims that Casciato will put the pension funds into risky hedge funds, but the person running Casciato’s campaign disagrees.

Political consultant Jim Ross, who is working on the campaign pro bono for Casciato, said it’s a shoestring affair and accusations of risky investments strategies by his opponent are false.

“This is not a big effort in terms of money spent,” said Ross.

Casciato told the Examiner that the campaign has spent about $40,000 so far, but would not say how much has been raised.

“I think this is an attempt by him to create a false difference,” Casciato said of his opponent.

Casicato defended himself when it came to allegations of the public safety cabal.

“It’s a very false argument to say that this is a public safety take over and that [public] safety will have an undue influence.” said Casciato.

Meiberger, who said he’s only spent about $12,000 of his own funds for mailers, argued meanwhile that his expertise far outstrips Casciato.

“There’s been a lot of misinformation spread by my opponent,” said Meiberger. “If we have some big hedge fund losses…the taxpayers are going to have to cough up.”

Election

The election is open to the roughly 60,000 pensioners and current city employees. Voting began in mid-December.

Unlike public elections, SFPERS board members are only required to file a few of the transparency filings others are, and only if they are a city employee, according to the San Francisco Ethics Commission.

NO MORE HEDGE FUNDS At SFERS: SFPOA, IFPE 21 Muscat & MEA Stop The Power Grab For SFERS!

https://youtu.be/AmCuJceKQcI

On December 27, 2016, a press conference and rally was held outside the offices of the San Francisco Police Officer Association SFPOA. The SFPOA, the Municipal Executives Association MEA and IFPTE Local 21 are making a power grab to take total control of the SF city employees pension fund and turn 25% or more of the funds into hedge funds. They are also trying to bully candidate Herb Meiberger and City and County employees to give them control of the pension fund.

Participants talked about the role of speculative hedge funds and the efforts to put police and firemen in charge of the pension funds regardless of their small number of participants.

Also there is growing evidence of pension spiking of the SFERS by member Joseph Driscoll and SFPOA SFERS candidate Capt. Al Casciato who retired as a captain with a base salary of $118,000 and now receives a yearly pension of $208,000 a year. Members of the MEA and top officials of CCSF departments have been manipulating the SFES pension fund to personally benefit themselves which is not only unethical but likely illegal as well as threatening the integrity of the funds.

SFERS board member and Lt. SFFD Joseph Driscoll also attended the rally and holed up at the Turtle Tower Vietnamese restaurant across the street where he was trying to surreptitiously take pictures of the press conference. One wonders if he was on the city payroll and building up more overtime for his retirement from the city by spying on those who are trying to protect their pensions from more hedge fund deals.

The event was sponsored by the United Public Workers For Action http://www.upwa.info

For more media:

https://youtu.be/bGSaSG5EiME

http://sfbamo.com/news/fear-and-finance-in-saint-francis-police-and-the-politics-of-city-pension-reform-part-1/

http://www.stoplhhdownsize.com/What_Price_for_a_Seat_at_the_Retirement_Board_Table.pdf

http://www.ibtimes.com/san-francisco-hedge-fund-proposal-raises-conflict-interest-questions-1700230

http://www.pionline.com/article/20140609/PRINT/306099987/buffetts-suggestion-to-pension-fund-trustee-dont-invest-in-hedge-funds

https://www.indybay.org/newsitems/2016/12/02/18794329.php

http://www.wsj.com/articles/teachers-union-and-hedge-funds-war-over-pension-billions-1467125055

http://blog.sfgate.com/cityinsider/2014/12/15/financial-questions-dog-former-sf-first-lady-wendy-paskin-jordan/

http://code.socialdashboard.com/news/investment-by-san-francisco-pension-official-raises-questions-about-favors

https://www.youtube.com/watch?v=bjznPAFcCNE&feature=youtu.be

http://youtu.be/dCz5eMvYPBA

https://www.youtube.com/watch?v=Exbl3wwBx9Y

https://www.youtube.com/watch?v=p6VTO4UHrjk

https://soundcloud.com/workweek-radio/ww12-23-14-sf-public-pensions-with-david-sirota-ca-dir-secret-confernce

http://www.sfchronicle.com/bayarea/article/Ties-questioned-for-financial-adviser-and-former-5959036.php

http://www.aft.org/sites/default/files/allthatglittersisnotgold2015.pdf

For more information on Herb Meiberger

http://herbmeiberger.com

http://1021.seiu.org/page/-/ReElectHerbMeiberger-SFERSBoard.pdf

Production of Labor Video Project

http://www.laborvideo.org

SFERS Bosses Harass Retirees & Workers Protesting 25% Hedge Fund Investments

https://youtu.be/C2-KvH8E-T8

On Wednesday January 11, 2017 before a meeting of the San Francisco Employee Retirement System Board, CCSF workers and retirees protested and spoke out against the effort to grab control of the pension fund by the San Francisco Police Officers Association SFPOA, IFPTE Local 21 and the Municipal Executive Association MEA. While speaking and leafletting in front of the building the SFERS management arranged to have the building superintendent harass and threaten them. The police were called two times in an effort to stop the leafletting and speak out in front of the meeting. The effort to pack the board with police an firemen and exclude the only miscellaneous employee representative and CFT Herb Meiberger is being funded by hundreds of thousands of dollars of secret funds that don't have to be reported and are being sent to a corporate lawyer.

CALPERS and the New York public pension system have removed any investments in hedge funds because of the highly speculative nature of the investments and massive fees for speculators.

For more information on Herb Meiberger

http://herbmeiberger.com

http://1021.seiu.org/…/-/ReElectHerbMeiberger-SFERSBoard.pdf

Additional media:

https://youtu.be/bGSaSG5EiME

http://sfbamo.com/…/fear-and-finance-in-saint-francis-poli…/

http://www.stoplhhdownsize.com/What_Price_for_a_Seat_at_the…

http://www.ibtimes.com/san-francisco-hedge-fund-proposal-ra…

http://www.pionline.com/…/buffetts-suggestion-to-pension-fu…

https://www.indybay.org/newsitems/2016/12/02/18794329.php

http://www.wsj.com/…/teachers-union-and-hedge-funds-war-ove…

http://blog.sfgate.com/…/financial-questions-dog-former-sf…/

http://code.socialdashboard.com/…/investment-by-san-francis…

https://www.youtube.com/watch?v=bjznPAFcCNE&feature=youtu.be

http://youtu.be/dCz5eMvYPBA

https://www.youtube.com/watch?v=Exbl3wwBx9Y

https://www.youtube.com/watch?v=p6VTO4UHrjk

https://soundcloud.com/…/ww12-23-14-sf-public-pensions-with…

http://www.sfchronicle.com/…/Ties-questioned-for-financial-…

http://www.aft.org/…/default/files/allthatglittersisnotgold…

Production of Labor Video Project

http://www.laborvideo.org

The party is over for hedge funds. And the hangover could hurt

http://money.cnn.com/2016/05/18/investing/hedge-fund-golden-age-over-fees/index.html

by Matt Egan @mattmegan5

May 18, 2016: 12:18 PM ET

<160518105015-jim-chanos-salt-780x439.jpg>

The hedge fund industry's golden age of fat fees and superior returns is over. And the future looks decidedly less fun.

The hedge-fund managers who take home billions of dollars in pay are no longer in denial. There was somber acceptance at last week's SALT hedge fund conference in Las Vegas that fees need to go down.

"The fees are ridiculous," billionaire hedge-fund manager Jim Chanos told reporters at SALT, a swanky annual conference held at the Bellagio. "I'm shocked they stayed this high for this long."

Powered by SmartAsset.com

SMARTASSET.COM

And Leon Cooperman, the billionaire founder of hedge fund Omega Advisors, said the $3 trillion hedge fund industry's business model is "under assault."

What's the problem? Hedge funds just aren't crushing it on returns any more. A barometer of hedge fund performance, called the HFRI Fund Weighted Composite Index, has generated an annualized gain of just 1.7% over the past five years. Compared to that, the S&P 500's average annualized return for the same period was 11%.

However, hedge funds charge huge fees that eat into client returns. The standard fee structure, known as "two and twenty," calls for a flat 2% fee on total assets managed and an additional 20% on profits earned.

Related: Hedge fund kings made less last year

Now hedge funds are facing a revolt from the asset managers who used to steer vast sums of money their way. For example, in 2014 the largest U.S. pension fund, the California Public Employees' Retirement System (CalPERS) ditched hedge funds entirely.

Roslyn Zhang, managing director of the massive sovereign wealth fund China Investment Corporation, said she is "disappointed" in the performance of hedge funds her firm uses. Zhang, whose CIC manages $200 billion, criticized hedge funds for adopting "herd mentality" of making similar bets.

"Should we pay 'two and twenty' to be treated like this? Maybe we are not making the right decision," she said.

Others are asking the same question. Hedge fund clients yanked $15.1 billion in just the first three months of this year, according to research firm HFR. That marked the largest outflow since 2009.

As they shift away from "active" investing, investors continue to pour money into "passive" strategies. Over the past three years equity ETFs have enjoyed a $405 billion surge of inflows, according to research firm XTF.

These passive strategies are paying off. About 85% of actively-managed large cap equity funds trailed the S&P 500 over the past five years, according to S&P Dow Jones Indices.

Related: George Soros bets big...on gold

Another challenge for hedge funds: many markets tend to move in the same direction these days. That "correlation" between asset classes -- even ones with little in common -- makes it tougher for hedge fund managers to beat the markets.

For instance, in February, there were a couple of weeks when oil and the S&P 500 moved in lockstep 96% of the time. That's abnormal, given that there's been almost no correlation between stock and oil prices in the past decade.

"I've never seen correlation like this," said Emanuel Friedman, CEO of hedge fund EJF Capital. "We've never had this virtuous circle where all six or seven things interact with each other."

There are also regulatory challenges on the horizon for hedge funds. All three remaining U.S. presidential candidates have proposed ending the carried-interest tax loophole, under which hedge fund managers pay a lower tax on their gains than what regular folks pay on income.

Despite lower returns for the industry overall, some hedge fund superstars are still raking in boatloads of cash. The top 25 hedge fund managers earned a combined $13 billion last year,according to Institutional Investor's Alpha. But even that's down from 2013 when they pulled in more than $21 billion.

Related: Political fear is paralyzing investors

So what does the future look like for hedge funds?

It's not clear what fee structure will be deemed the "right" one in today's world. Something that rewards outperformance could make sense.

But lower fees is sure to drive poor performing hedge funds out of the business. "There becomes a point of equilibrium where it's not profitable to run a hedge fund," said Kenneth Tropin, founder of Graham Capital Management.

The challenging political and market environment means the hedge fund industry should "reduce its profile," said Joseph Brusuelas, chief economist at RSM, a major sponsor of SALT.

"It might be a good idea to tone it down. I'll leave it at that," he said.

Hedge Fund Math: Heads We Win, Tails You Lose

Common Sense

http://www.nytimes.com/2016/12/22/business/hedge-fund-fees-returns.html?ref=business

By JAMES B. STEWART

DEC. 22, 2016

Thanks to William A. Ackman’s early successes, his longtime investors have fared much better than the more recent ones. CreditDrew Angerer for The New York Times

When do 1.5 and 16 add up to 72?

That’s the riddle confronting investors in Pershing Square Holdings Ltd., the closed-end fund run by the prominent activist investor Bill Ackman.

In a letter to investors this month, Mr. Ackman disclosed that through the end of November, the fund had declined 13.5 percent this year after accounting for fees. (Pershing Square Holdings shouldn’t be confused with Pershing Square L.P., Mr. Ackman’s hedge fund, although the two vehicles have the same investment strategy.)

That’s obviously a big disappointment, considering the Standard & Poor’s 500-stock index was up 7.6 percent over the same period. But that’s not what some big investors were complaining about to me this week.

In the same letter, Mr. Ackman reported that during the nearly four years since it began, Pershing Square Holdings had gained a total of 20.5 percent. That would be considered mediocre at best, considering the S.&P. 500 gained over 67 percent during the same period.

And that’s a 20.5 percent gain before deducting fees. Pershing Square Holdings charges investors a 1.5 percent management fee and takes 16 percent of any gains. After those fees were deducted, investors gained just 5.7 percent.

That means Pershing Square kept approximately 72 percent of the fund’s gains for itself, leaving investors with the measly remains.

A spokesman for Mr. Ackman declined to comment. But the reality is that many hedge funds, not just Mr. Ackman’s, reap far higher percentages of their gains than that stated in their fee structure. That’s because when they experience substantial losses — as Pershing Square did last year and is on track to do this year (its year-to-date loss through Tuesday was 12.4 percent) — they don’t have to give anything back.

And for many hedge funds the results are even worse. Most hedge funds charge the proverbial two-and-20 — 2 percent of assets under management and 20 percent of any gains above a certain threshold. By these measures, Pershing Square Holdings’ lower fee structure is a relative bargain.

How could Pershing Square have kept 72 percent of the gains, given that its fee structure calls for a performance fee of just 16 percent?

The answer can be found in relatively simple math. As a simple example, consider an investment of $1 million in a fund that generates a 10 percent return in years one and two and then loses 5 percent in years three and four. The investor would end up with about $1.09 million, a total gain of $90,000, or 9 percent, over the four years before fees.

But now consider the return after deducting a 20 percent performance fee. In years one and two, the fund manager earns $20,000 and $20,400 for a total of $40,400. The fund’s manager earns nothing in years three and four. After deducting the fees, the investor would end up after the four years with just $1.05 million, a total return of 5 percent. But the $40,400 earned by the fund is nearly 45 percent of the investor’s total gains before fees — not 20 percent. (And that’s not even figuring in a 1.5 or 2 percent management fee.)

If the losses are big enough, the hedge fund manager can capture 100 percent of the gross return, or investors can lose money even as fund managers line their pockets.

Investors seem to be finally catching on to the fact that most hedge fund managers share generously in the good times, but are exposed to none of the losses in bad.

Because of concerns over high fees and disappointing results, some endowments and pension funds, including those in Illinois, New Jersey and Rhode Island, have cut back substantially on their hedge fund allocations this year, following the lead of Calpers, the largest pension fund in the United States, which said in 2014 that it would exit hedge funds entirely.

Through the third quarter of this year, investors had withdrawn about $51.5 billion from hedge funds, according to Hedge Fund Research.

“I’ve been saying for some time that the two-and-20 model is dead,” said Christopher J. Ailman, chief investment officer for the California State Teachers Retirement System, which manages assets of close to $200 billion.

“Take the Pershing Square example,” he said. “Investors are only capturing 28 percent of the gains, which is totally out of whack. If it were my money, I’d say it should be the other way around — the investors should be keeping 70 percent, or even more, like 75 to 80 percent. That’s what I’d consider fair.”

Mr. Ailman said that he and the chief investment officers for several large pension funds were seeking an alternative fee structure that would preserve a performance incentive for managers but more equitably share the risk. “A few very big states are really thinking through this,” he said.

One approach under consideration, he said, is to use a rolling multiyear period for measuring performance fees. In year one, for example, an investor would pay only a portion of the performance fee if there was a gain. If there were losses in subsequent years, the investor would claw back the withheld compensation. That would solve the Pershing Square Holdings problem. “Quite a few large investors are thinking along these lines,” Mr. Ailman told me. “Of course the devil is in the details.”

Such an approach is anathema to most hedge funds, which rely on annual performance fees to compensate their highly paid — some would say overpaid — staffs.

Even so, hedge funds are competing more fiercely over fees. In a nod to investor concerns, earlier this year Mr. Ackman offered investors an option to pay no performance fees on gains of less than 5 percent, but a steeper 30 percent on gains above that level.

“Management fees pretty much used to be 2 percent,” Mr. Ailman said. “Now we’re seeing them as low as 70 basis points.” And performance fees, known as carried interest, have dropped in some cases from 20 percent “to the low teens and even as low as 10 percent. And these are large, well-known funds.”

Hedge fund defenders have said it isn’t fair to pick just four years of performance, like the Pershing Square Holdings example, saying it is too short a track record. Thanks to Mr. Ackman’s early successes, his longtime investors have fared much better than the more recent ones, and cumulative fees are closer to the percentages in the stated fee structures.

In his letter to investors, Mr. Ackman pointed to much better results for his older hedge fund, Pershing Square L.P. Since it started in 2004, it has produced annualized compounded returns after fees of 14.9 percent, more than double the S.&P. 500’s 7.6 percent.

Still, he acknowledged, “while this is a good result, it is below our long-term goals and not much solace” for “investors who joined us in recent years.”

NYCERS pulls the plug on hedge funds "As trustees of the New York City Employees' Retirement System voted last week to liquidate its hedge fund holdings, the nation's largest public pension fund shared an update of its own exit plans: CalPERS has reduced its hedge fund investments by more than 80% since divulging plans to divest."

http://www.pionline.com/article/20160418/PRINT/304189975/nycers-pulls-the-plug-on-hedge-funds

BY ROBERT STEYER | APRIL 18, 2016

Scott Stringer said an asset allocation without hedge funds will allow NYCERS to meet its long-term objectives.

As trustees of the New York City Employees' Retirement System voted last week to liquidate its hedge fund holdings, the nation's largest public pension fund shared an update of its own exit plans: CalPERS has reduced its hedge fund investments by more than 80% since divulging plans to divest.

With its announcement on April 14, NYCERS became the latest large public plan to reduce or eliminate hedge fund holdings, an investment that has drawn fire from critics over disappointing returns, lack of transparency and fees.

Hedge funds represent about 2.8% of NYCERS' total pension fund assets of $51.2 billion.

In approving the hedge fund resolution, NYCERS trustees noted that the fund's consultant, San Francisco-based Callan Associates, conducted a review that “demonstrated that hedge funds can be removed from the NYCERS asset mix to achieve targeted levels of return and maintain consistent levels of volatility.”

“We have not seen the results that we had expected,” said trustee Henry Garrido. Mr. Garrido, who offered the resolution, is executive director of District Council 37, American Federation of State, County and Municipal Employees.

NYCERS started investing in hedge funds in March 2011. Its hedge fund portfolio's annualized return for the three years ended June 30, 2015, was 6.54% gross of fees, compared to the benchmark 7.29% gross of fees, according to NYCERS' latest annual report.

Plan trustees didn't set a timetable for disposing of the $1.45 billion in hedge fund assets the fund held as of Jan. 31, 2016, recommending that liquidation take place “as soon as practicable, in an orderly and prudent manner.”

Could take some time

Based on CalPERS' experience, liquidating the NYCERS portfolio could take some time.

CalPERS announced in September 2014 that it would eliminate its $4 billion hedge fund program, citing complexity, cost and scale. Hedge funds then represented about 1.3% of CalPERS' assets.

As of Dec. 31, 2015, the $290.7 billion California Public Employees' Retirement System, Sacramento, held only $463 million in hedge fund investments.

“The program has been eliminated and staff reassigned,” Joe DeAnda, a spokesman, wrote in an e-mail.

CalPERS said at the time that the process would take about a year. But as Mr. DeAnda noted in his e-mail, “the one year exit timeline was always an estimate.”

Mr. DeAnda didn't provide information on where the hedge fund money was reassigned, except to say liquidated funds “get reinvested into the portfolio according to our asset allocation targets.”

Unions have been among the fiercest hedge fund critics.

The American Federation of Teachers co-authored a report in November recommending that 11 large public pension plans conduct asset allocation reviews to find “less costly and more effective diversification approaches” than hedge funds.

The report, co-authored by the Roosevelt Institute, identified NYCERS, the New York State Common Retirement Fund, Albany; the Employees' Retirement System of Rhode Island, Providence; the Massachusetts Pension Reserves Investment Management Board, Boston; and the Illinois State Board of Investment, Chicago, as among large public pension plans that should revisit their hedge-fund investing strategy.

Representatives from the Rhode Island, Massachusetts and New York State pension systems did not respond to requests for comment about whether they were reviewing their hedge fund investments.

The Illinois State Board of Investment announced in February it would lower its hedge fund allocation target to 3% from the current 10%.

In March, the board said it would launch nine separate RFPs for equity and bond managers totaling $3.2 billion. Most of the funding will come from terminating equity, fixed-income and hedge fund-of-funds managers, the board said.

Reducing hedge fund exposure to a 3% allocation could take 12 to 18 months, William Atwood, the board's executive director, told Pensions & Investments in March.

The AFT-Roosevelt Institute report also recommended that the New Jersey Pension Fund, Trenton, review its asset allocation strategy and hedge-fund investments to find “less costly and more effective diversification approaches.”

Last month, a coalition of public employee unions issued a report criticizing performance and fees for the $68.1 billion New Jersey pension fund's alternatives investments such as hedge funds and private equity. Hedge funds represented 12.4% of the total pension assets, as of Feb. 29.

The division of investment, which manages investments for the New Jersey fund, responded last month that this report contained “numerous” inaccuracies, unclear calculations and a “significant amount” of data mining and cherry-picking.

“The view that has been expressed by the State Treasury Department, Division of Investment, State Investment Council and nearly all industry experts is that a diverse portfolio, including hedge fund investments, mitigates risk and produces the best returns for beneficiaries over a substantial period of time,” said Christopher Santarelli, a Treasury Department spokesman, in an e-mail.

“We wish that the partisan groups leading the charge against these investments would not prioritize politics over what is best for the financial security of public pension fund beneficiaries,” he added.

In New York City, NYCERS is one of three city pension funds investing in hedge funds.

As of Jan. 31, the New York City Police Pension Fund had $1.04 billion in hedge fund assets out of a total $31.6 billion, and the New York City Fire Department Pension Fund had $335 million in hedge fund assets out of a total $10.36 billion. Representatives of the police and fire department funds declined to comment on whether their trustees are reviewing their hedge fund investments.

The Teachers' Retirement System of the City of New York and the New York City Board of Education Retirement System don't invest in hedge funds.

Each city pension fund has its own board of trustees. The five funds are part of the $154 billion New York City Retirement Systems.

Among the 11 NYCERS trustees, 10 voted on April 14 to get out of hedge funds.

Trustee Letitia James, the New York City public advocate and the city's second-highest ranking elected official, seconded the resolution. At the meeting, Ms. James criticized what she said were “exorbitant” fees being paid for “high-risk and opaque investments.” Ms. James said she saw “little evidence” that the hedge fund portfolio added overall value via increased returns or decreased risk.

Responsible portfolio

In a statement issued after the meeting, New York City Comptroller Scott Stringer, who is the fiduciary for the five New York City pension funds, said the trustees believe an asset allocation without hedge funds will help NYCERS “construct a responsible portfolio that meets our long-term investment objectives.” The trustees have not yet voted on a revised asset allocation strategy.

The one dissenting vote on hedge fund divestmentcame from Patricia Stryker, recording secretary, Local 237, of the International Brotherhood of Teamsters, representing Gregory Floyd, a NYCERS trustee and president of Local 237. Ms. Stryker said her union believes it would be “premature” for NYCERS to exit hedge funds now. Given NYCERS' strategy of investing for the long term, “we haven't been in hedge funds that long” to make a comprehensive assessment, she said.

As of June 30, NYCERS had hedge investments with Brevan Howard, Brigade Capital Management, Carlson Capital, Caspian Capital, Cantab Capital Partners, D.E. Shaw, Fir Tree Partners, Luxor Capital Group, Perry Capital, Pharo Management, SRS Investment Management, Standard General and Turiya Capital.

This article originally appeared in the April 18, 2016 print issue as, "NYCERS pulls the plug on hedge funds".

— Contact Robert Steyer at rsteyer [at] pionline.com | @Steyer_P

San Francisco Employees’ Retirement Board Member Herb Meiberger poses for a portrait Tuesday, January 3, 2016. (Jessica Christian/S.F. Examiner)

By Jonah Owen Lamb on January 15, 2017 1:00 am

The election for a seat on a little-known body that has power over billions of dollars in investments is getting ugly and the results could impact thousands of San Francisco pensioners, city coffers and taxpayers.

But no one knows how much money is being spent or who is paying for the campaign, which has prompted Supervisor Malia Cohen to introduce a drafting request for legislation that would require transparency in such elections.

But for now, this fight over a seat on the San Francisco Employee Retirement System will remain in the dark even though the seven-member body — three mayoral appointees, three elected seats and one Board of Supervisors appointee — collectively vote on how more than $20 billion in pension funds are invested.

So far, the two candidates — one a former cop and the other an incumbent and former city employee — have thrown accusations at one another in an uncommonly expensive race (almost $50,000 has been spent so far) that has included a protest in front of the San Francisco Police Officer Association and that body’s vocal support for one candidate.

Former SFPERS board member and retired police officer Al Casciato said he was called on by a number of city unions to run for the seat in order to remove the incumbent, who his campaign has called divisive and overcautious, and whose actions have already impacted the fund’s bottom line.

Herb Meiberger, the incumbent whose terms ends Feb. 20 and who worked for The City advising it on investing, has served on the SFPERS board for 24 years, said his role has been to keep steady the finances of the fund.

Meiberger has cast his opponent as a big spending police and fire union-backed candidate set on making riskier bets with the billions in investment dollars the retirement board controls.

Casciato’s election, Meiberger added, would put all three elected board members into the hands of public safety-linked members, which in other cities has not worked out well for pensioners.

The truth, at least the facts that can been pinned down in an election for which only public employees and retirees can vote and that is not required to be transparent like elections for public office, lies somewhere in between these narratives.

This all matters to city voters because the fund’s ultimate performance will be a major factor in how much The City must pay out in pensions.

The City projects a deficit of $119 million in the next fiscal year and $283 million in the subsequent fiscal year, which is driven largely by pensions and payroll. Those pension costs are projected to rise; by fiscal year 2021-22 The City expects to spend $431 million in pensions, $171 million more than previously expected.

The fund

The fund was valued at $21 billion as of fiscal year 2016-15, which is nearly $5 billion more than it was valued at in 2011-12.

Still, several recent years of less-than-robust gains have meant increased contributions from employees and The City.

This issue of how well the fund has been performing is at the heart of this divisive election, said Patrick Monette-Shaw in a recent San Francisco Examiner opinion article on the matter.

“They’re lying to frighten voters into voting for Casciato to invest more of SFERS’ $21 billion portfolio in high-risk hedge funds,” the West Side Observer columnist wrote.

But not everyone is siding with Meiberger, the incumbent.

A video attacking Meiberger on the POA’s website says his obstructionism has lost the fund money and cost benefits.

The candidates

Meiberger claims that Casciato will put the pension funds into risky hedge funds, but the person running Casciato’s campaign disagrees.

Political consultant Jim Ross, who is working on the campaign pro bono for Casciato, said it’s a shoestring affair and accusations of risky investments strategies by his opponent are false.

“This is not a big effort in terms of money spent,” said Ross.

Casciato told the Examiner that the campaign has spent about $40,000 so far, but would not say how much has been raised.

“I think this is an attempt by him to create a false difference,” Casciato said of his opponent.

Casicato defended himself when it came to allegations of the public safety cabal.

“It’s a very false argument to say that this is a public safety take over and that [public] safety will have an undue influence.” said Casciato.

Meiberger, who said he’s only spent about $12,000 of his own funds for mailers, argued meanwhile that his expertise far outstrips Casciato.

“There’s been a lot of misinformation spread by my opponent,” said Meiberger. “If we have some big hedge fund losses…the taxpayers are going to have to cough up.”

Election

The election is open to the roughly 60,000 pensioners and current city employees. Voting began in mid-December.

Unlike public elections, SFPERS board members are only required to file a few of the transparency filings others are, and only if they are a city employee, according to the San Francisco Ethics Commission.

NO MORE HEDGE FUNDS At SFERS: SFPOA, IFPE 21 Muscat & MEA Stop The Power Grab For SFERS!

https://youtu.be/AmCuJceKQcI

On December 27, 2016, a press conference and rally was held outside the offices of the San Francisco Police Officer Association SFPOA. The SFPOA, the Municipal Executives Association MEA and IFPTE Local 21 are making a power grab to take total control of the SF city employees pension fund and turn 25% or more of the funds into hedge funds. They are also trying to bully candidate Herb Meiberger and City and County employees to give them control of the pension fund.

Participants talked about the role of speculative hedge funds and the efforts to put police and firemen in charge of the pension funds regardless of their small number of participants.

Also there is growing evidence of pension spiking of the SFERS by member Joseph Driscoll and SFPOA SFERS candidate Capt. Al Casciato who retired as a captain with a base salary of $118,000 and now receives a yearly pension of $208,000 a year. Members of the MEA and top officials of CCSF departments have been manipulating the SFES pension fund to personally benefit themselves which is not only unethical but likely illegal as well as threatening the integrity of the funds.

SFERS board member and Lt. SFFD Joseph Driscoll also attended the rally and holed up at the Turtle Tower Vietnamese restaurant across the street where he was trying to surreptitiously take pictures of the press conference. One wonders if he was on the city payroll and building up more overtime for his retirement from the city by spying on those who are trying to protect their pensions from more hedge fund deals.

The event was sponsored by the United Public Workers For Action http://www.upwa.info

For more media:

https://youtu.be/bGSaSG5EiME

http://sfbamo.com/news/fear-and-finance-in-saint-francis-police-and-the-politics-of-city-pension-reform-part-1/

http://www.stoplhhdownsize.com/What_Price_for_a_Seat_at_the_Retirement_Board_Table.pdf

http://www.ibtimes.com/san-francisco-hedge-fund-proposal-raises-conflict-interest-questions-1700230

http://www.pionline.com/article/20140609/PRINT/306099987/buffetts-suggestion-to-pension-fund-trustee-dont-invest-in-hedge-funds

https://www.indybay.org/newsitems/2016/12/02/18794329.php

http://www.wsj.com/articles/teachers-union-and-hedge-funds-war-over-pension-billions-1467125055

http://blog.sfgate.com/cityinsider/2014/12/15/financial-questions-dog-former-sf-first-lady-wendy-paskin-jordan/

http://code.socialdashboard.com/news/investment-by-san-francisco-pension-official-raises-questions-about-favors

https://www.youtube.com/watch?v=bjznPAFcCNE&feature=youtu.be

http://youtu.be/dCz5eMvYPBA

https://www.youtube.com/watch?v=Exbl3wwBx9Y

https://www.youtube.com/watch?v=p6VTO4UHrjk

https://soundcloud.com/workweek-radio/ww12-23-14-sf-public-pensions-with-david-sirota-ca-dir-secret-confernce

http://www.sfchronicle.com/bayarea/article/Ties-questioned-for-financial-adviser-and-former-5959036.php

http://www.aft.org/sites/default/files/allthatglittersisnotgold2015.pdf

For more information on Herb Meiberger

http://herbmeiberger.com

http://1021.seiu.org/page/-/ReElectHerbMeiberger-SFERSBoard.pdf

Production of Labor Video Project

http://www.laborvideo.org

SFERS Bosses Harass Retirees & Workers Protesting 25% Hedge Fund Investments

https://youtu.be/C2-KvH8E-T8

On Wednesday January 11, 2017 before a meeting of the San Francisco Employee Retirement System Board, CCSF workers and retirees protested and spoke out against the effort to grab control of the pension fund by the San Francisco Police Officers Association SFPOA, IFPTE Local 21 and the Municipal Executive Association MEA. While speaking and leafletting in front of the building the SFERS management arranged to have the building superintendent harass and threaten them. The police were called two times in an effort to stop the leafletting and speak out in front of the meeting. The effort to pack the board with police an firemen and exclude the only miscellaneous employee representative and CFT Herb Meiberger is being funded by hundreds of thousands of dollars of secret funds that don't have to be reported and are being sent to a corporate lawyer.

CALPERS and the New York public pension system have removed any investments in hedge funds because of the highly speculative nature of the investments and massive fees for speculators.

For more information on Herb Meiberger

http://herbmeiberger.com

http://1021.seiu.org/…/-/ReElectHerbMeiberger-SFERSBoard.pdf

Additional media:

https://youtu.be/bGSaSG5EiME

http://sfbamo.com/…/fear-and-finance-in-saint-francis-poli…/

http://www.stoplhhdownsize.com/What_Price_for_a_Seat_at_the…

http://www.ibtimes.com/san-francisco-hedge-fund-proposal-ra…

http://www.pionline.com/…/buffetts-suggestion-to-pension-fu…

https://www.indybay.org/newsitems/2016/12/02/18794329.php

http://www.wsj.com/…/teachers-union-and-hedge-funds-war-ove…

http://blog.sfgate.com/…/financial-questions-dog-former-sf…/

http://code.socialdashboard.com/…/investment-by-san-francis…

https://www.youtube.com/watch?v=bjznPAFcCNE&feature=youtu.be

http://youtu.be/dCz5eMvYPBA

https://www.youtube.com/watch?v=Exbl3wwBx9Y

https://www.youtube.com/watch?v=p6VTO4UHrjk

https://soundcloud.com/…/ww12-23-14-sf-public-pensions-with…

http://www.sfchronicle.com/…/Ties-questioned-for-financial-…

http://www.aft.org/…/default/files/allthatglittersisnotgold…

Production of Labor Video Project

http://www.laborvideo.org

The party is over for hedge funds. And the hangover could hurt

http://money.cnn.com/2016/05/18/investing/hedge-fund-golden-age-over-fees/index.html

by Matt Egan @mattmegan5

May 18, 2016: 12:18 PM ET

<160518105015-jim-chanos-salt-780x439.jpg>

The hedge fund industry's golden age of fat fees and superior returns is over. And the future looks decidedly less fun.

The hedge-fund managers who take home billions of dollars in pay are no longer in denial. There was somber acceptance at last week's SALT hedge fund conference in Las Vegas that fees need to go down.

"The fees are ridiculous," billionaire hedge-fund manager Jim Chanos told reporters at SALT, a swanky annual conference held at the Bellagio. "I'm shocked they stayed this high for this long."

Powered by SmartAsset.com

SMARTASSET.COM

And Leon Cooperman, the billionaire founder of hedge fund Omega Advisors, said the $3 trillion hedge fund industry's business model is "under assault."

What's the problem? Hedge funds just aren't crushing it on returns any more. A barometer of hedge fund performance, called the HFRI Fund Weighted Composite Index, has generated an annualized gain of just 1.7% over the past five years. Compared to that, the S&P 500's average annualized return for the same period was 11%.

However, hedge funds charge huge fees that eat into client returns. The standard fee structure, known as "two and twenty," calls for a flat 2% fee on total assets managed and an additional 20% on profits earned.

Related: Hedge fund kings made less last year

Now hedge funds are facing a revolt from the asset managers who used to steer vast sums of money their way. For example, in 2014 the largest U.S. pension fund, the California Public Employees' Retirement System (CalPERS) ditched hedge funds entirely.

Roslyn Zhang, managing director of the massive sovereign wealth fund China Investment Corporation, said she is "disappointed" in the performance of hedge funds her firm uses. Zhang, whose CIC manages $200 billion, criticized hedge funds for adopting "herd mentality" of making similar bets.

"Should we pay 'two and twenty' to be treated like this? Maybe we are not making the right decision," she said.

Others are asking the same question. Hedge fund clients yanked $15.1 billion in just the first three months of this year, according to research firm HFR. That marked the largest outflow since 2009.

As they shift away from "active" investing, investors continue to pour money into "passive" strategies. Over the past three years equity ETFs have enjoyed a $405 billion surge of inflows, according to research firm XTF.

These passive strategies are paying off. About 85% of actively-managed large cap equity funds trailed the S&P 500 over the past five years, according to S&P Dow Jones Indices.

Related: George Soros bets big...on gold

Another challenge for hedge funds: many markets tend to move in the same direction these days. That "correlation" between asset classes -- even ones with little in common -- makes it tougher for hedge fund managers to beat the markets.

For instance, in February, there were a couple of weeks when oil and the S&P 500 moved in lockstep 96% of the time. That's abnormal, given that there's been almost no correlation between stock and oil prices in the past decade.

"I've never seen correlation like this," said Emanuel Friedman, CEO of hedge fund EJF Capital. "We've never had this virtuous circle where all six or seven things interact with each other."

There are also regulatory challenges on the horizon for hedge funds. All three remaining U.S. presidential candidates have proposed ending the carried-interest tax loophole, under which hedge fund managers pay a lower tax on their gains than what regular folks pay on income.

Despite lower returns for the industry overall, some hedge fund superstars are still raking in boatloads of cash. The top 25 hedge fund managers earned a combined $13 billion last year,according to Institutional Investor's Alpha. But even that's down from 2013 when they pulled in more than $21 billion.

Related: Political fear is paralyzing investors

So what does the future look like for hedge funds?

It's not clear what fee structure will be deemed the "right" one in today's world. Something that rewards outperformance could make sense.

But lower fees is sure to drive poor performing hedge funds out of the business. "There becomes a point of equilibrium where it's not profitable to run a hedge fund," said Kenneth Tropin, founder of Graham Capital Management.

The challenging political and market environment means the hedge fund industry should "reduce its profile," said Joseph Brusuelas, chief economist at RSM, a major sponsor of SALT.

"It might be a good idea to tone it down. I'll leave it at that," he said.

Hedge Fund Math: Heads We Win, Tails You Lose

Common Sense

http://www.nytimes.com/2016/12/22/business/hedge-fund-fees-returns.html?ref=business

By JAMES B. STEWART

DEC. 22, 2016

Thanks to William A. Ackman’s early successes, his longtime investors have fared much better than the more recent ones. CreditDrew Angerer for The New York Times

When do 1.5 and 16 add up to 72?

That’s the riddle confronting investors in Pershing Square Holdings Ltd., the closed-end fund run by the prominent activist investor Bill Ackman.

In a letter to investors this month, Mr. Ackman disclosed that through the end of November, the fund had declined 13.5 percent this year after accounting for fees. (Pershing Square Holdings shouldn’t be confused with Pershing Square L.P., Mr. Ackman’s hedge fund, although the two vehicles have the same investment strategy.)

That’s obviously a big disappointment, considering the Standard & Poor’s 500-stock index was up 7.6 percent over the same period. But that’s not what some big investors were complaining about to me this week.

In the same letter, Mr. Ackman reported that during the nearly four years since it began, Pershing Square Holdings had gained a total of 20.5 percent. That would be considered mediocre at best, considering the S.&P. 500 gained over 67 percent during the same period.

And that’s a 20.5 percent gain before deducting fees. Pershing Square Holdings charges investors a 1.5 percent management fee and takes 16 percent of any gains. After those fees were deducted, investors gained just 5.7 percent.

That means Pershing Square kept approximately 72 percent of the fund’s gains for itself, leaving investors with the measly remains.

A spokesman for Mr. Ackman declined to comment. But the reality is that many hedge funds, not just Mr. Ackman’s, reap far higher percentages of their gains than that stated in their fee structure. That’s because when they experience substantial losses — as Pershing Square did last year and is on track to do this year (its year-to-date loss through Tuesday was 12.4 percent) — they don’t have to give anything back.

And for many hedge funds the results are even worse. Most hedge funds charge the proverbial two-and-20 — 2 percent of assets under management and 20 percent of any gains above a certain threshold. By these measures, Pershing Square Holdings’ lower fee structure is a relative bargain.

How could Pershing Square have kept 72 percent of the gains, given that its fee structure calls for a performance fee of just 16 percent?

The answer can be found in relatively simple math. As a simple example, consider an investment of $1 million in a fund that generates a 10 percent return in years one and two and then loses 5 percent in years three and four. The investor would end up with about $1.09 million, a total gain of $90,000, or 9 percent, over the four years before fees.

But now consider the return after deducting a 20 percent performance fee. In years one and two, the fund manager earns $20,000 and $20,400 for a total of $40,400. The fund’s manager earns nothing in years three and four. After deducting the fees, the investor would end up after the four years with just $1.05 million, a total return of 5 percent. But the $40,400 earned by the fund is nearly 45 percent of the investor’s total gains before fees — not 20 percent. (And that’s not even figuring in a 1.5 or 2 percent management fee.)

If the losses are big enough, the hedge fund manager can capture 100 percent of the gross return, or investors can lose money even as fund managers line their pockets.

Investors seem to be finally catching on to the fact that most hedge fund managers share generously in the good times, but are exposed to none of the losses in bad.

Because of concerns over high fees and disappointing results, some endowments and pension funds, including those in Illinois, New Jersey and Rhode Island, have cut back substantially on their hedge fund allocations this year, following the lead of Calpers, the largest pension fund in the United States, which said in 2014 that it would exit hedge funds entirely.

Through the third quarter of this year, investors had withdrawn about $51.5 billion from hedge funds, according to Hedge Fund Research.

“I’ve been saying for some time that the two-and-20 model is dead,” said Christopher J. Ailman, chief investment officer for the California State Teachers Retirement System, which manages assets of close to $200 billion.

“Take the Pershing Square example,” he said. “Investors are only capturing 28 percent of the gains, which is totally out of whack. If it were my money, I’d say it should be the other way around — the investors should be keeping 70 percent, or even more, like 75 to 80 percent. That’s what I’d consider fair.”

Mr. Ailman said that he and the chief investment officers for several large pension funds were seeking an alternative fee structure that would preserve a performance incentive for managers but more equitably share the risk. “A few very big states are really thinking through this,” he said.

One approach under consideration, he said, is to use a rolling multiyear period for measuring performance fees. In year one, for example, an investor would pay only a portion of the performance fee if there was a gain. If there were losses in subsequent years, the investor would claw back the withheld compensation. That would solve the Pershing Square Holdings problem. “Quite a few large investors are thinking along these lines,” Mr. Ailman told me. “Of course the devil is in the details.”

Such an approach is anathema to most hedge funds, which rely on annual performance fees to compensate their highly paid — some would say overpaid — staffs.

Even so, hedge funds are competing more fiercely over fees. In a nod to investor concerns, earlier this year Mr. Ackman offered investors an option to pay no performance fees on gains of less than 5 percent, but a steeper 30 percent on gains above that level.

“Management fees pretty much used to be 2 percent,” Mr. Ailman said. “Now we’re seeing them as low as 70 basis points.” And performance fees, known as carried interest, have dropped in some cases from 20 percent “to the low teens and even as low as 10 percent. And these are large, well-known funds.”

Hedge fund defenders have said it isn’t fair to pick just four years of performance, like the Pershing Square Holdings example, saying it is too short a track record. Thanks to Mr. Ackman’s early successes, his longtime investors have fared much better than the more recent ones, and cumulative fees are closer to the percentages in the stated fee structures.

In his letter to investors, Mr. Ackman pointed to much better results for his older hedge fund, Pershing Square L.P. Since it started in 2004, it has produced annualized compounded returns after fees of 14.9 percent, more than double the S.&P. 500’s 7.6 percent.

Still, he acknowledged, “while this is a good result, it is below our long-term goals and not much solace” for “investors who joined us in recent years.”

NYCERS pulls the plug on hedge funds "As trustees of the New York City Employees' Retirement System voted last week to liquidate its hedge fund holdings, the nation's largest public pension fund shared an update of its own exit plans: CalPERS has reduced its hedge fund investments by more than 80% since divulging plans to divest."

http://www.pionline.com/article/20160418/PRINT/304189975/nycers-pulls-the-plug-on-hedge-funds

BY ROBERT STEYER | APRIL 18, 2016

Scott Stringer said an asset allocation without hedge funds will allow NYCERS to meet its long-term objectives.

As trustees of the New York City Employees' Retirement System voted last week to liquidate its hedge fund holdings, the nation's largest public pension fund shared an update of its own exit plans: CalPERS has reduced its hedge fund investments by more than 80% since divulging plans to divest.

With its announcement on April 14, NYCERS became the latest large public plan to reduce or eliminate hedge fund holdings, an investment that has drawn fire from critics over disappointing returns, lack of transparency and fees.

Hedge funds represent about 2.8% of NYCERS' total pension fund assets of $51.2 billion.

In approving the hedge fund resolution, NYCERS trustees noted that the fund's consultant, San Francisco-based Callan Associates, conducted a review that “demonstrated that hedge funds can be removed from the NYCERS asset mix to achieve targeted levels of return and maintain consistent levels of volatility.”

“We have not seen the results that we had expected,” said trustee Henry Garrido. Mr. Garrido, who offered the resolution, is executive director of District Council 37, American Federation of State, County and Municipal Employees.

NYCERS started investing in hedge funds in March 2011. Its hedge fund portfolio's annualized return for the three years ended June 30, 2015, was 6.54% gross of fees, compared to the benchmark 7.29% gross of fees, according to NYCERS' latest annual report.

Plan trustees didn't set a timetable for disposing of the $1.45 billion in hedge fund assets the fund held as of Jan. 31, 2016, recommending that liquidation take place “as soon as practicable, in an orderly and prudent manner.”

Could take some time

Based on CalPERS' experience, liquidating the NYCERS portfolio could take some time.

CalPERS announced in September 2014 that it would eliminate its $4 billion hedge fund program, citing complexity, cost and scale. Hedge funds then represented about 1.3% of CalPERS' assets.

As of Dec. 31, 2015, the $290.7 billion California Public Employees' Retirement System, Sacramento, held only $463 million in hedge fund investments.

“The program has been eliminated and staff reassigned,” Joe DeAnda, a spokesman, wrote in an e-mail.

CalPERS said at the time that the process would take about a year. But as Mr. DeAnda noted in his e-mail, “the one year exit timeline was always an estimate.”

Mr. DeAnda didn't provide information on where the hedge fund money was reassigned, except to say liquidated funds “get reinvested into the portfolio according to our asset allocation targets.”

Unions have been among the fiercest hedge fund critics.

The American Federation of Teachers co-authored a report in November recommending that 11 large public pension plans conduct asset allocation reviews to find “less costly and more effective diversification approaches” than hedge funds.

The report, co-authored by the Roosevelt Institute, identified NYCERS, the New York State Common Retirement Fund, Albany; the Employees' Retirement System of Rhode Island, Providence; the Massachusetts Pension Reserves Investment Management Board, Boston; and the Illinois State Board of Investment, Chicago, as among large public pension plans that should revisit their hedge-fund investing strategy.

Representatives from the Rhode Island, Massachusetts and New York State pension systems did not respond to requests for comment about whether they were reviewing their hedge fund investments.

The Illinois State Board of Investment announced in February it would lower its hedge fund allocation target to 3% from the current 10%.

In March, the board said it would launch nine separate RFPs for equity and bond managers totaling $3.2 billion. Most of the funding will come from terminating equity, fixed-income and hedge fund-of-funds managers, the board said.

Reducing hedge fund exposure to a 3% allocation could take 12 to 18 months, William Atwood, the board's executive director, told Pensions & Investments in March.

The AFT-Roosevelt Institute report also recommended that the New Jersey Pension Fund, Trenton, review its asset allocation strategy and hedge-fund investments to find “less costly and more effective diversification approaches.”

Last month, a coalition of public employee unions issued a report criticizing performance and fees for the $68.1 billion New Jersey pension fund's alternatives investments such as hedge funds and private equity. Hedge funds represented 12.4% of the total pension assets, as of Feb. 29.

The division of investment, which manages investments for the New Jersey fund, responded last month that this report contained “numerous” inaccuracies, unclear calculations and a “significant amount” of data mining and cherry-picking.

“The view that has been expressed by the State Treasury Department, Division of Investment, State Investment Council and nearly all industry experts is that a diverse portfolio, including hedge fund investments, mitigates risk and produces the best returns for beneficiaries over a substantial period of time,” said Christopher Santarelli, a Treasury Department spokesman, in an e-mail.

“We wish that the partisan groups leading the charge against these investments would not prioritize politics over what is best for the financial security of public pension fund beneficiaries,” he added.

In New York City, NYCERS is one of three city pension funds investing in hedge funds.

As of Jan. 31, the New York City Police Pension Fund had $1.04 billion in hedge fund assets out of a total $31.6 billion, and the New York City Fire Department Pension Fund had $335 million in hedge fund assets out of a total $10.36 billion. Representatives of the police and fire department funds declined to comment on whether their trustees are reviewing their hedge fund investments.

The Teachers' Retirement System of the City of New York and the New York City Board of Education Retirement System don't invest in hedge funds.

Each city pension fund has its own board of trustees. The five funds are part of the $154 billion New York City Retirement Systems.

Among the 11 NYCERS trustees, 10 voted on April 14 to get out of hedge funds.

Trustee Letitia James, the New York City public advocate and the city's second-highest ranking elected official, seconded the resolution. At the meeting, Ms. James criticized what she said were “exorbitant” fees being paid for “high-risk and opaque investments.” Ms. James said she saw “little evidence” that the hedge fund portfolio added overall value via increased returns or decreased risk.

Responsible portfolio

In a statement issued after the meeting, New York City Comptroller Scott Stringer, who is the fiduciary for the five New York City pension funds, said the trustees believe an asset allocation without hedge funds will help NYCERS “construct a responsible portfolio that meets our long-term investment objectives.” The trustees have not yet voted on a revised asset allocation strategy.

The one dissenting vote on hedge fund divestmentcame from Patricia Stryker, recording secretary, Local 237, of the International Brotherhood of Teamsters, representing Gregory Floyd, a NYCERS trustee and president of Local 237. Ms. Stryker said her union believes it would be “premature” for NYCERS to exit hedge funds now. Given NYCERS' strategy of investing for the long term, “we haven't been in hedge funds that long” to make a comprehensive assessment, she said.

As of June 30, NYCERS had hedge investments with Brevan Howard, Brigade Capital Management, Carlson Capital, Caspian Capital, Cantab Capital Partners, D.E. Shaw, Fir Tree Partners, Luxor Capital Group, Perry Capital, Pharo Management, SRS Investment Management, Standard General and Turiya Capital.

This article originally appeared in the April 18, 2016 print issue as, "NYCERS pulls the plug on hedge funds".

— Contact Robert Steyer at rsteyer [at] pionline.com | @Steyer_P

For more information:

http://www.sfexaminer.com/divisive-electio...

Add Your Comments

We are 100% volunteer and depend on your participation to sustain our efforts!

Donate

$140.00 donated

in the past month

Get Involved

If you'd like to help with maintaining or developing the website, contact us.

Publish

Publish your stories and upcoming events on Indybay.

Topics

More

Search Indybay's Archives

Advanced Search

►

▼

IMC Network